Developing and maintaining proper insurance to value has been a constant struggle for many organizations. The largest inflation in 40 years is one of the factors causing underinsurance and gaps in insurance. A report by Altus Group suggests that up to 75% of commercial properties may be underinsured, leaving businesses exposed to significant financial risks. Risk assessment firm AIR Worldwide reports that 34.6% of insurable North American average annual loss (AAL) is uninsured, resulting in an estimated $32.7 billion in unreimbursed cost to policyholders.

Replacement cost for insurance purposes is not developed in the normal preparation of business financial statements. The starting value is one of the largest issues with inadequate property valuations. How are property values reported? How are they developed? What is the methodology in developing values each year? Are values static or are they being adjusted for increases/decreases in costs? In this blog post, we’ll attempt to answer these questions.

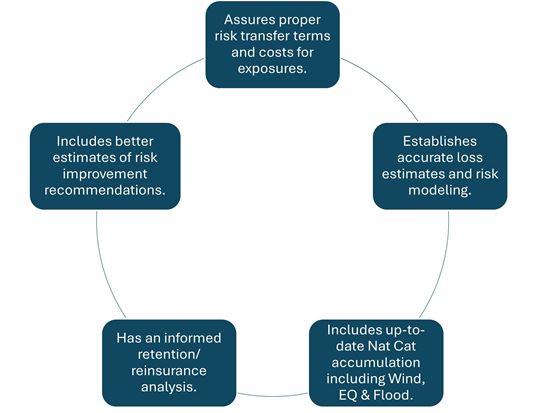

Due diligence builds a trusting relationship with all parties. Failure to report adequate values can create issues in the insurance decision-making process. To help mitigate the risk related to undervaluation, insurers are using coinsurance clauses. Coinsurance clauses apply limits on a location basis, including margin clauses, opt out of renewals, etc. Successful property insurance programs include a common element: a thorough and responsive system for establishing and reporting up-to-date insurable values.

Having accurate values can also help with risk assessments for loss scenarios. With reliable values, loss scenarios become more accurate, better model expected losses and provide correct coverage. Developing and maintaining accurate property replacement values is a fundamental operation every business should conduct to ensure their assets and property are sufficiently insured.

Maintaining your values is an important aspect. Here are tips on keeping your values current:

In 2020, The Capital One Bank Tower in Lake Charlies, LA suffered a loss due to Hurricane Laura. The 22-story, 400,000 sq. ft., building was an iconic skyscraper for the city. After the hurricane, the building remained vacant and unusable until 2024, where it was finally demolished. An investigation by The Real Deal revealed that building owner Hertz Investment Group placed the fair value of the 22-story building at $25 million in 2019 but estimated that they needed $140 million for the damages. The loss “jeopardized Hertz’s cash flows and financial position and impeded Hertz’s ability to tap the bond market for liquidity,” the publication reported.

As we can see, undervaluation can have a big impact on a business. This situation could possibly have been avoided by doing a benchmark or $/SF analysis. The reported value of $63/SF would raise a red flag that the reported value appears to be understated.

Interested in learning more about insurance asset valuation and protecting against underinsurance? We invite you to watch our recent webinar: Inflation and Property Valuation, featuring Justin Chen, Global Manager, Valuation Services, Global Risk Consultants; Charlie Carriker, Strategic Sales Manager-Project Services, Global Risk Consultants; and Frank Francone, Senior Director Risk Management, Brookfield Properties.

Site Selector

Global

Americas

Asia

Europe

Middle East and Africa